Your Khums, Explained Simply

Each year, you set aside 20% of your surplus wealth, what remains after your expenses. This simple act purifies your earnings and connects you to those who need it most.

Sehme Imam

50% to Maraja for community & religious needs

Sehme Sadaat

50% to needy Sadaat: orphans, widows & more

Lives You've Changed

What Your Khums Supports

Every pound you give becomes food, shelter, and hope for families who have no one else to turn to.

Widows & Orphans Assistance

Providing essential support, housing, and monthly stipends to vulnerable families who have lost their breadwinners.

Religious Education & Community Outreach

Funding Islamic seminaries, educational programs, and community centers that nurture faith and knowledge.

Emergency Relief

Delivering urgent food, shelter, and medical aid to communities affected by crisis and natural disasters.

In 2025, donors like you made incredible things possible.

Need Help With Your Khums?

Calculating Khums can feel overwhelming, especially if it's your first time. Our friendly team is here to walk you through every step. We'll help you work out your Khums date, understand what counts as surplus, and answer any questions you have. No pressure, no judgement.

Frequently Asked Questions

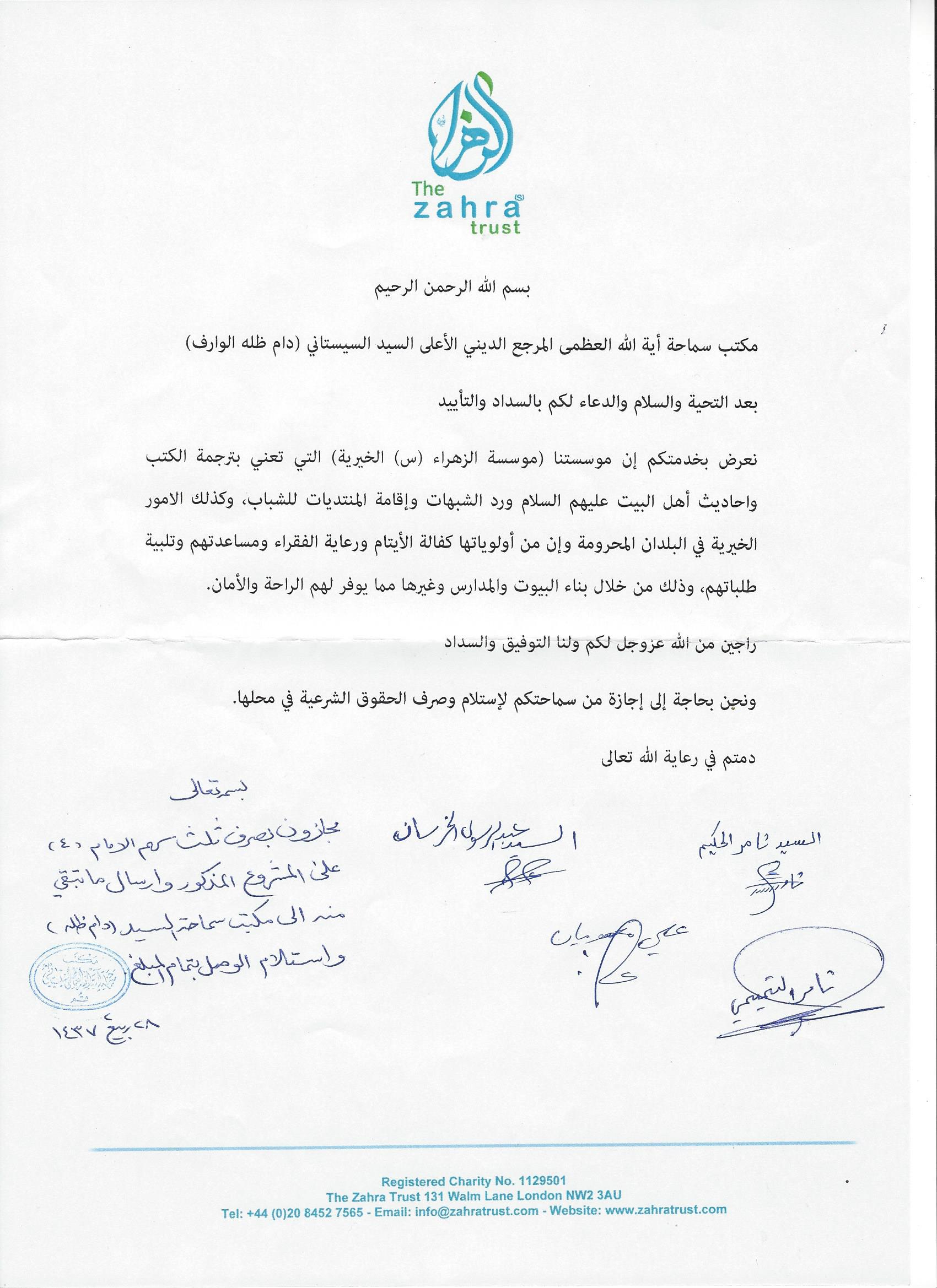

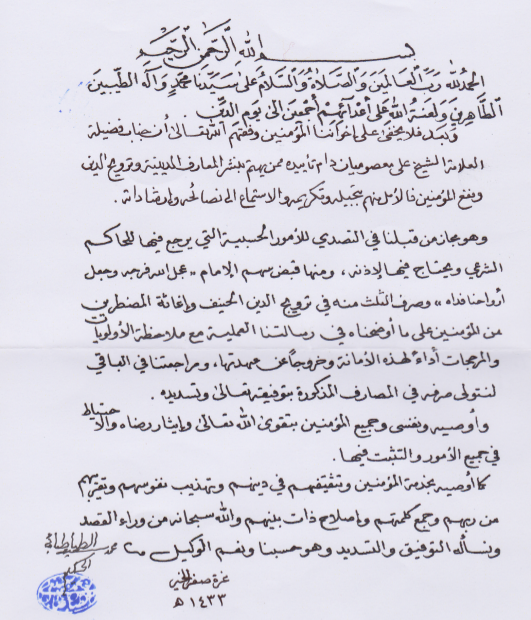

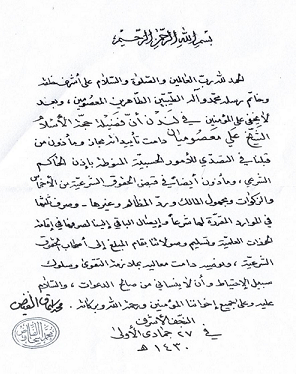

Based on Islamic jurisprudence and the rulings of leading Shia scholars (Maraja), including His Eminence Ayatullah Sayyid Ali al-Sistani.

-

What is Khums in Islam?

Khums is a religious obligation in Islam, especially emphasized in Shia Islam, which requires eligible believers to contribute 20% (one-fifth) of their surplus income at the end of the year towards specified causes. In practical terms, after you subtract all your living expenses for the year, if you have savings or profit remaining, one-fifth of that amount is due as Khums. It is one of the Furūʿ al-Dīn (ancillaries of the faith) in Ja’fari Shia jurisprudence, alongside duties like prayer and Zakat. The payment of Khums serves to purify one’s wealth and is a form of support for the community, as the collected funds are used for the welfare of society and for the descendants of the Prophet (saww).

-

Who is eligible to pay Khums?

Every Muslim who is ‘baligh’ (mature/adult) and financially stable enough to have savings at their year-end should assess if Khums is due. In essence, if after a year you have surplus money or goods that are beyond your necessary expenses, then Khums becomes obligatory on that surplus. This obligation is most prominently observed by followers of the Ahlulbayt (as) (Shia Muslims who follow the guidance of the Maraja). If you are unsure about your status, it’s recommended to consult your Marja or a knowledgeable scholar. Request a callback and our team at The Zahra Trust can help determine your Khums liability.

-

How is Khums different from Zakat?

While both Khums and Zakat are forms of obligatory charity in Islam, they have different scopes and rates. Zakat (for those required to pay it) is usually 2.5% of certain types of wealth (such as cash, gold/silver above a threshold, business goods, agricultural produce, etc.) and it has a defined list of eligible recipients. Khums, on the other hand, is 20% of surplus wealth (savings/profit) after all expenses, and it is primarily mandated in Shia Islamic law. Another key difference is in the allocation: Zakat can be given to any deserving Muslim in the eight categories mentioned in the Quran, whereas Khums is split into Sehme Imam (used for community and religious causes under scholar supervision) and Sehme Sadaat (given to needy descendants of the Prophet (saww)). Some individuals may end up paying both Zakat and Khums if they meet the criteria for each.

-

What are Sehme Imam and Sehme Sadaat?

These are the two components of Khums. Sehme Imam means ‘the share of the Imam.’ In the absence of the Imam (during the Occultation of the 12th Imam (ajtfs) in Shia belief), this share is entrusted to the Maraja (high-ranking jurists) to spend in ways that would please the Imam (ajtfs). Practically, Sehme Imam funds are used for things like supporting religious seminaries, building or maintaining mosques and community centers, funding humanitarian relief for oppressed or needy Shia communities. Sehme Sadaat means ‘the share of the Sadaat (Prophet (saww)’s descendants).’ The Prophet (saww)’s family (Banu Hashim) does not receive Zakat, so Sehme Sadaat is reserved for aiding Sayyids who are poor, orphaned, widowed, or otherwise in need. At The Zahra Trust, we separate and distribute these shares under the oversight of qualified scholars.

-

Do all Shias pay Khums?

All Shia Ithna-‘Ashari Muslims who have surplus income after annual expenses are obligated to pay Khums. However, not everyone has surplus. If your total income equals your necessary expenses, there is no Khums. Some Shias unfortunately do not pay due to ignorance or negligence. The Imams never suspended this obligation; it has been wajib at all times. As Imam al-Mahdi (ajtfs) stated: ‘Whosoever uses our property without our permission is cursed, and on the Day of Judgement we will be his opponent.’ (Al-Ihtijaj, Sheikh al-Tabarsi)

-

Why do Sunni Muslims not pay Khums?

This is based on a difference in interpretation of the Qur’anic verse (8:41). Sunni Muslims generally restrict Khums to specific cases like war booty, while Shia Muslims (following the Ja’fari school) apply it to yearly savings/profits as well. In Arabic, al-ghanimah has two meanings: spoils of war AND profit/earnings generally. The Prophet (saww) himself collected Khums from the gains of Yemeni Muslims when no war had occurred. The Imams of Ahlulbayt (as) consistently taught that Khums applies to annual surplus income, and this interpretation is followed by Shia Muslims based on authentic traditions from the Prophet (saww)’s family.

-

Is Khums a charity or a duty?

Unlike voluntary charity (sadaqa), Khums is an obligatory act for those who meet the criteria. It is not optional for eligible believers. Allah (swt) ordained Khums to protect the rights of the oppressed and to ensure the dignity of the Prophet (saww)’s family is maintained. The Prophet Muhammad (saww) famously forbade his close relatives from accepting Zakat, likening such charity for them to an impurity. Instead, Allah allocated a share of certain wealth to them through Khums. This is a system designed by Allah (swt) to uplift, empower, and preserve the community.

-

When should I pay Khums?

Khums becomes wajib at the beginning of your new financial year on the profit or surplus of the past year’s income. You are allowed to fix any day of the year as the ‘beginning’, for example, the start of a fiscal year, the Hijri calendar, or the day you started earning. You then count the surplus of your income on that day annually and pay Khums. However, Khums is actually associated with profit as soon as it is known, and you may pay before year end if you wish.

-

Do you pay Khums if you have debt?

Only debts for essential needs can be deducted from income before calculating Khums, not debts for expanding business or investments. In the latter case, you must first pay Khums from the surplus of your income, then pay such debts from the remaining 80%. If there is a decrease in your capital during the year, you are permitted to make it up by deducting that amount from the profit before paying Khums. Not sure how debt affects your Khums?

-

Is there a minimum amount to pay Khums?

There is no minimum threshold for Khums like there is for Zakat. If you have any surplus after deducting your annual living expenses, 20% of that surplus is liable for Khums. Even small amounts of savings are subject to Khums. The manner and amount of your expenditure should be considered according to your needs and status. If you exceed your reasonable limit, the excess counts as savings. If your total income equals your necessary expenses, there is no Khums.

-

Can Khums be backdated?

Yes, if you have never paid Khums in previous years despite being eligible, you are still obligated to pay it for those past years. This process is sometimes called ‘backdating’ Khums or paying retroactive Khums. Essentially, you would calculate, for each year missed, what your surplus income was for that year and then set aside 20% for Khums. It’s recommended to work with a scholar or our team to calculate backdated Khums correctly. Get help calculating backdated Khums → Once paid, you will have ‘cleansed’ that portion of your wealth and can start fresh with a regular annual Khums schedule.

-

What counts as income for Khums purposes?

Income means whatever you earn from business, wage or salary, dividend income, or by other means of possession recognized by the shari’ah. According to most present Maraja, it is precautionarily wajib to pay Khums from gifts, prizes, legacy (bequests from non-relatives), charity, Zakat and Khums received. However, Khums is not liable on dowry (mahr) or inheritance, except when one inherits from a very remote relative.

-

What expenses can I deduct before calculating Khums?

Deductible household expenses include: food, drink, accommodation, transportation, furniture, marriage expenses, medical expenses, payment of sadaqah, hajj, ziyarat, gifts, donations and charity, paying debts for essential needs, legal penalties, wages of servants, insurance premiums (car, fire, medical, protection), mandatory pension/provident fund deductions, and income tax. Note: permanent life insurance premiums and non-mandatory retirement savings are not deductible. They are savings liable for Khums. Use our calculator for accurate deductions

-

What about items not used by year end?

All new items that have not been used (even once) by the end of your Khums year must be counted as your savings. For example, if you have unused food items like sugar, salt, or rice remaining at year end, you cannot deduct their price from income. They must be included in calculating your annual savings and are liable for Khums. Include everything in your calculation

-

Do I need to pay Khums on gold and jewellery?

The ruling varies based on usage. Personal jewelry worn regularly for adornment may be exempt if used within the year, as it counts as part of household consumption. However, gold kept as investment or savings, or new jewelry not worn by year end, is considered savings and is liable for Khums. Consult with our team for your specific situation

-

What if my wealth is mixed with illegitimate earnings?

If legitimate wealth is mixed with illegitimate wealth (from usury, gambling, etc.) and you cannot distinguish the amounts: pay Khums from the entire wealth to make it lawful. If you know the amount but not the owner: give that amount as charity (sadaqah) on behalf of the unknown owner, with permission from your Marja. If you know the owner but not the amount: come to a compromise with the owner. If you know both: return the property to its rightful owner. Need guidance? Request a callback

-

What is Khums GCSE?

In GCSE Religious Studies, Khums is taught as one of the Ten Obligatory Acts in Shia Islam. Students learn that Khums means ‘one-fifth’, that is 20% of surplus annual income that Shia Muslims must pay. It is divided into two halves: Sehme Imam (for religious leaders and institutions) and Sehme Sadaat (for descendants of the Prophet (saww) who are in need). GCSE courses explain how Khums differs from Zakat and its role in supporting the Muslim community.

-

How do I pay Khums through The Zahra Trust?

You can fulfill your Khums obligation safely and securely through The Zahra Trust. Visit our Khums page where you will find detailed information and an online form. Complete the Khums form with your details and the amount you are paying. If you need help calculating the exact amount, you can use our Khums calculator. We can also help with obtaining any required religious permission (ijaza) if your Marja requires individual consent for Khums distribution. You can donate the Khums amount online. We accept card payments and bank transfers. The Zahra Trust will provide you with a receipt for your records. We hold ijaza from top Shia scholars (including Ayatullah Sistani) to collect and distribute Khums. Pay your Khums now

-

How is Khums used by The Zahra Trust?

The Zahra Trust is authorized by leading Shia scholars (Maraja), including His Eminence Ayatullah Sayyid Ali al-Sistani, to collect and distribute Khums funds. The Sehme Imam portion is used, with the permission of your Marja, to support community welfare and faith-based projects: providing food, clean water, housing, and medical aid to orphans, widows, refugees and others in crisis, as well as sponsoring Islamic education in under-resourced areas. The Sehme Sadaat portion is distributed directly to deserving Sadaat (needy members of the Prophet (saww)’s family), including impoverished Sayyid families, orphans and widows of noble lineage, to assist with their basic needs. Your Khums entrusted to us will go toward providing food, water, and shelter to orphans and widows; supporting displaced families in crisis regions; and directly assisting Sadaat in need. Make a difference today

-

What happens if I don't pay my Khums?

Not paying Khums, Zakat or fitrah amounts to misappropriation of money that rightfully belongs to the Imam (ajtfs) and the needy, orphans and poor. Imam Ali (as) wrote sternly to an officer who misappropriated public funds: ‘Do you not believe in the Day of Judgement, or do you not fear the exaction of account?…How can you enjoy food and drink when you know that you are eating the unlawful?’ The Imam stated that even if his own sons Hasan and Husayn had done such a thing, there would be no leniency. This shows how seriously Islam treats these obligations. (Nahj al-Balagha, Letter 41) Start by calculating what you owe

Khums Calculator

Calculate your khums accurately based on Islamic jurisprudence

Need Help? Request a Callback

Choose your calculation method

Already know your totals? Enter them directly below for a quick calculation.